Business Income Tax

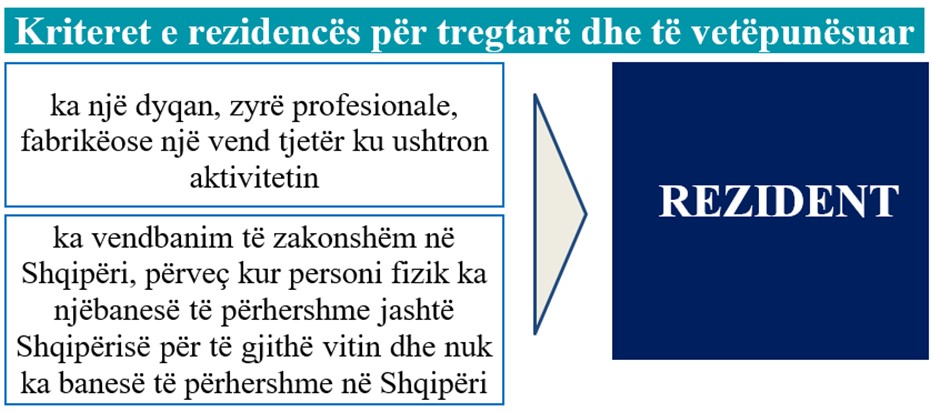

Residency – Personal Income Tax from Business

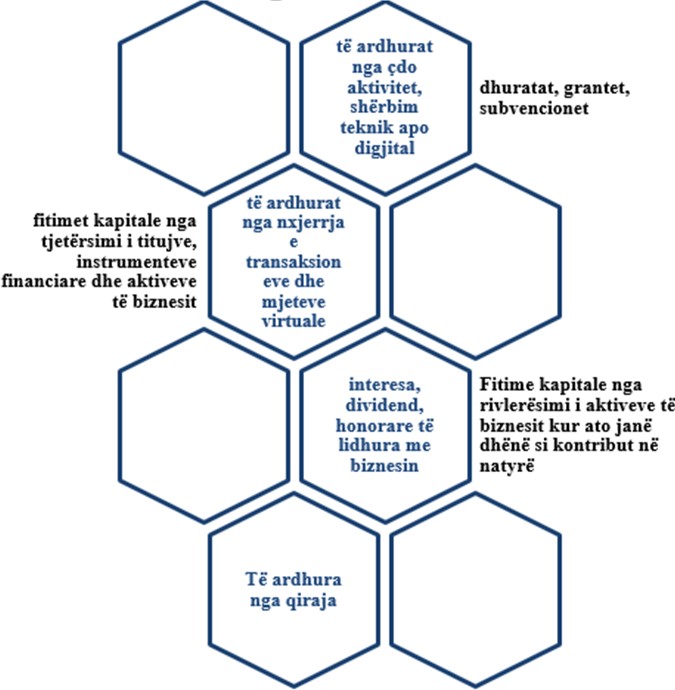

Business Income

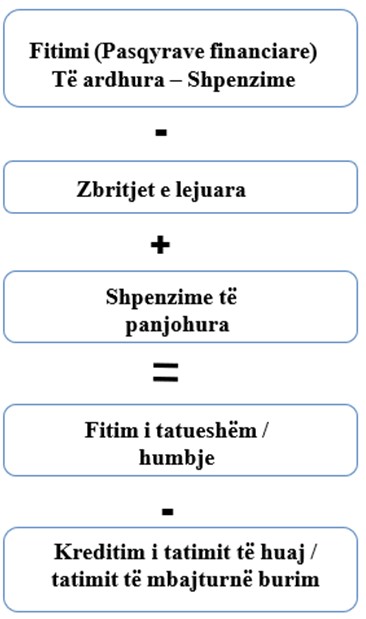

Calculation of Taxable Profit from Business According to Documents

Expenses for the purpose of:

Generating profit and in the interest of the business

Maintaining and securing income.

Expenses are documented by the taxpayer and are not subject to any limitation prescribed by this law

Rules for determining taxable profit according to Chapter IV for corporate tax.

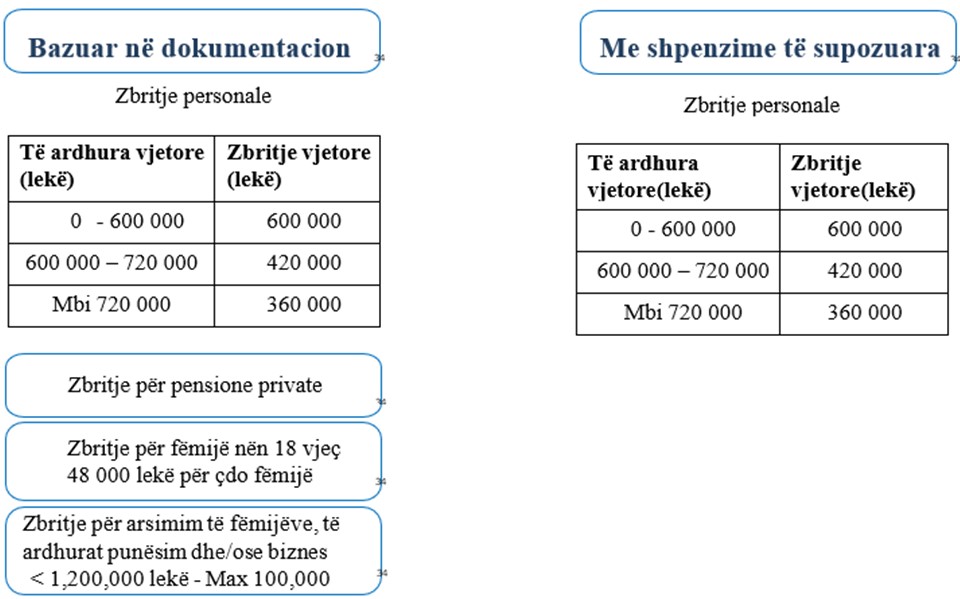

Allowed Deductions – Business Income

An individual is both employed (employment income) and registered as a sole proprietor (business income)

How often can they request personal deductions?

If only once, should personal deductions be applied in DIVA or in the business income declaration?

Can full personal deductions for the year be applied even if they did not work 12 months or were not active 12 months?

Where should deductions for private pension funds be applied: DIVA or business income declaration?

Where should deductions for children under 18 years be applied: DIVA or business income declaration?

Where should deductions for children's education be applied: DIVA or business income declaration?

For these and other questions, please contact us and we will assist you with any clarification.

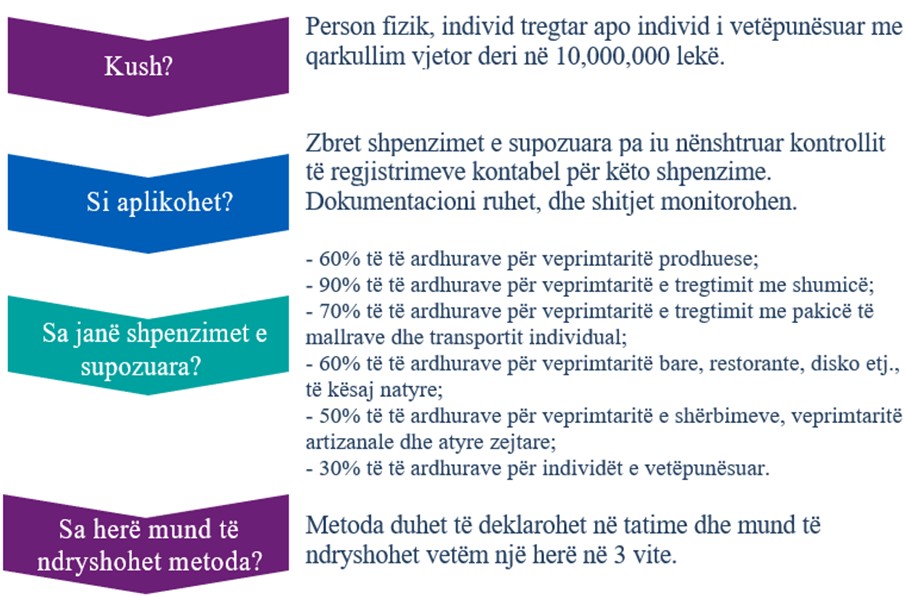

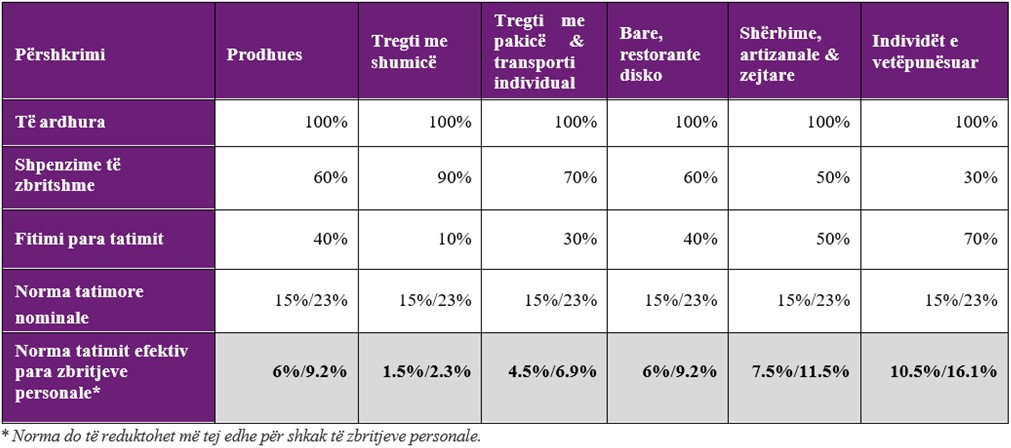

Special Regime – Presumed Expenses

Tax Rate

Traders, self-employed individuals, and entities with gross income up to 14 million ALL per year will benefit from a 0% personal income tax rate, applied until December 31, 2029. This 0% tax rate does not apply to self-employed individuals and entities providing professional services. The analytical list of professional services will be determined by a Council of Ministers Decision (VKM).

| Traders | Gross income over 14 million ALL per year | From 1.1.2024

|

||||||

| Self-Employed / Entities | a. Gross income over 14 million ALL per year, or b. Offer professional services (list via VKM, regardless of income) |

| Traders | Gross income up to 14 million ALL per year | From 1.1.2024 to 31.12.2029 0% |

| Self-Employed / Entities | a. Gross income up to 14 million ALL per year, or b. Do not offer professional services (list via VKM) |

Transition from Self-Employed to “Employee”

Declaration in the business income declaration by the self-employed.

Does not apply when 100% of income comes from non-residents or entities without a permanent establishment in Albania.

Comparison of Personal Income Tax Schemes for Business

Net Taxable Base

Self-employed / Professional services

Income: 9,000,000 ALL

Expenses: 4,000,000 ALL

Method: Documented expenses

Clients: Many

Status: Married with one child

Income: 9,000,000 ALL

Expenses: – 4,000,000 ALL

Personal deduction: – 360,000 ALL

Child deduction: – 48,000 ALL

Taxable Base: 4,592,000 ALL

Tax: 4,592,000 * 15% = 688,800 ALL

Net Presumed Taxable Base

Self-employed / Professional services

Income: 9,000,000 ALL

Expenses: 4,000,000 ALL

Method: Presumed expenses

Clients: Many

Status: Married with one child

Income: 9,000,000 ALL

Expenses: – 2,700,000 ALL

Personal deduction: – 360,000 ALL

Child deduction: – 0 ALL

Taxable Base: 5,940,000 ALL

Tax: 5,940,000 * 15% = 891,000 ALL

Gross Taxable Base

Self-employed / Professional services

Income: 9,000,000 ALL

Expenses: 4,000,000 ALL

Method: Documented expenses

Clients: One

Status: Married with one child

Income: 9,000,000 ALL

Expenses: – 0 ALL

Personal deduction: – 360,000 ALL

Child deduction: – 48,000 ALL

Taxable Base: 8,592,000 ALL

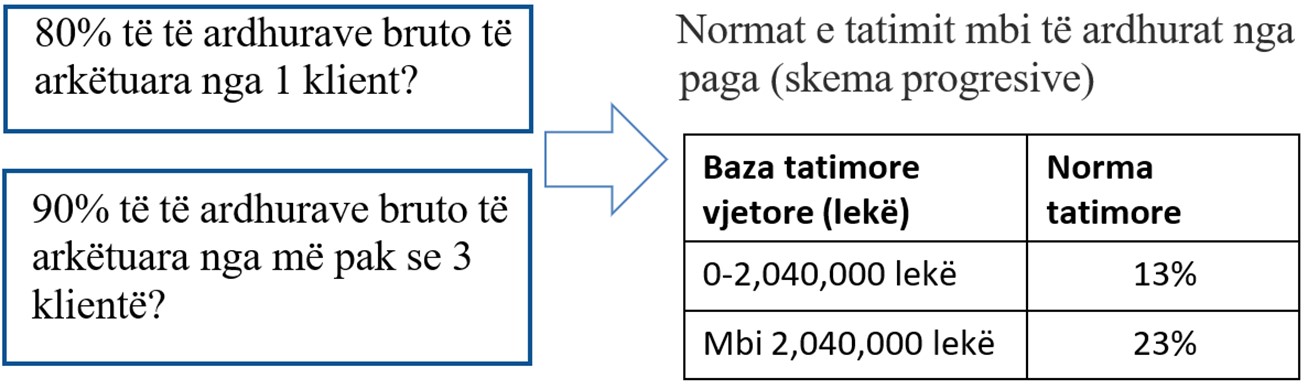

Tax: (8,592,000 – 2,040,000) * 23% + 2,040,000 * 13% = 1,772,160 ALL

Unknown Expenses

Costs of purchasing and improving land and construction sites.

Costs of purchase, improvement, renovation, and reconstruction of depreciable assets.

Depreciation expenses according to accounting rules.

Interest paid exceeding the 12-month average interest rate published by the Bank of Albania (except loans from microcredit institutions).

Fines and penalties.

Expenses for creating or increasing provisions, reserves, or other special funds.

Depreciation

Depreciation according to the accounting plan is deductible for personal income tax purposes.

Depreciation for fixed assets not used in business activity is not deductible.

Inventory

Inventory for business use must be recorded and valued according to accounting rules.

Excess or shortage of inventory is recognized as income or expense only if properly documented.

Bad Debt

Uncollectible receivables can be deducted only if written off in accounting records.

Provisioning for bad debts is limited to actual losses documented.

Prepayments

Prepaid expenses are deductible in the period in which they relate.

Advance payments for goods or services must be documented and matched with the period of benefit.

Carryforward of Losses

Losses from business activity can be carried forward for up to 5 years.

Only losses documented in accounting records and approved by tax authorities are allowed.

Business Income Declaration

Taxpayers must submit an annual business income declaration.

The declaration includes all income, expenses, deductions, and credits for the fiscal year.

It must be filed electronically through the tax authority portal.

Credit for Overpaid Tax

Any overpaid personal income tax can be carried forward as a credit against future tax liabilities.

Taxpayers can request a refund if the credit exceeds future liabilities.

Documentation – Personal Income Tax

All business income and expenses must be supported by proper accounting records and invoices.

Receipts, contracts, and other relevant documents must be retained for at least 5 years.

Reporting Obligations – Personal Income

Annual declaration of business income and any related tax payments.

Monthly or quarterly reporting may be required for withholding taxes, VAT, or other obligations.

Compliance with deadlines ensures avoidance of fines and interest charges.